The Passionate Investor Third Quarter 2020 and the Coronavirus Impact

The Passionate Investor Third Quarter 2020 and the Coronavirus Impact

Market Review

- Equity markets generally outperformed fixed-income markets with the S&P 500 rising 8.93% (including dividends; -5.57% YTD) and the Barclay’s Capital U.S. Aggregate Bond index increasing 0.62% (+6.79% YTD).

- Small caps underperformed large cap stocks (S&P 500) as the Russell 2000 small cap stock index returned +4.93% (-8.69% YTD).

- Value outperformed growth during the quarter (as determined by the S&P 1500 broad market index which includes large, mid, and small capitalization stocks).

- Non-U.S. equity markets underperformed U.S. markets in both U.S. dollar (MSCI EAFE**: +4.88% and -6.73% YTD) and local currency terms (+1.30% and -9.08% YTD, respectively).

- The MSCI Emerging Markets Index outperformed non-U.S. developed (international) markets. The index slightly underperformed U.S. stocks in local currency (8.79% and 2.93% YTD) but outperformed in USD (9.70% and -0.91% YTD).

- Most U.S. market sectors were positive. Consumer Discretionary (+15.06%; +23.38% YTD), Materials (+13.31%; +5.47% YTD), Industrial (+12.48%; -3.99% YTD), and Information Technology (+11.95%; +28.69% YTD) stocks were most distinguishable given their strength. The Energy sector was notable given its weakness (-19.72%; -48.09% YTD).

- High yield bonds climbed 4.28% (-0.58% YTD). The U.S. corporate bond sector rose 1.13% (+7.67% YTD). 10-Year U.S. Treasury yields experienced a slight increase from 0.65% at the beginning of the quarter to 0.66% currently (2.69% at the beginning of the year).

- The U.S. dollar fell versus the British Pound (-4.63%; +2.41% YTD), the Euro (-4.41%; -4.47% YTD), and Yen (-2.18%; -2.89% YTD).

* Unless otherwise noted, performances stated above reflect data provided by Standard and Poor’s, Russell Investments, MSCI, and Barclay’s Capital.

** The MSCI EAFE Index is a large capitalization, developed market benchmark that tracks non-U.S. or international equity markets.

Market Commentary

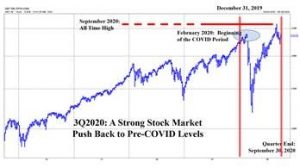

U.S. stocks rose 8.93% (the S&P 500), ending the quarter at essentially its pre-coronavirus level and with potentially its fastest recovery ever (+5.57% YTD). Indeed, that marker was breached earlier in September (see chart below) and the index remains within shouting distance of the all-time high. Still, the quarter was characterized by excessive volatility as investors contended with a second wave of COVID-19 cases, conflicting and moderating U.S. economic data, a lack of consensus as to a vaccine arrival date, failure by Congress to secure a second round of economic stimulus, and general uncertainty regarding the U.S. Presidential election in November. The U.S. Federal Reserve continued to be accommodative, even signaling that the current low interest rate regime may remain in place through 2024. Benchmark 10-Year U.S. Treasury bond yields remained flat and near their lowest level ever. Home prices, demand for homes generally, and mortgage refinancing activity have soared even as savers and fixed-income investors have struggled to earn good yields on everything from savings accounts to long-term bonds.

Small-cap and international (non-U.S. developed market) stocks came off their lofty second-quarter performance trajectory, climbing a more subdued 4.93% and 4.88% (in USD; respectively). Emerging market stocks kept pace with U.S. large caps, rising 8.79% in local currency and 9.70% in U.S. dollar terms. The U.S. Consumer Discretionary sector continued its strong ascent from the first quarter with a sector leading +15.06% second-quarter climb. The Energy sector was also quick to give up on its second-quarter gains, falling 19.72% as global demand for energy fell due to viral concerns and ensuing slower economic activity. Bonds offered a mixed bag as the Barclay’s Capital U.S. Aggregate Bond index increased 0.62% and credit sensitive sectors like high yield bonds climbed 4.28%. The U.S. dollar fell relative to most other currencies.

The commentary presented herein contains the opinions of Partnership Wealth Management, a registered investment advisor. This information should not be relied upon for tax purposes and is based upon sources believed to be reliable. No guarantee is made to the completeness or accuracy of this information. Partnership Wealth Management shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions contained herein or their use, which do not constitute investment advice, are provided as of the date written, are provided solely for informational purposes, and therefore are not an offer to buy or sell a security. Investments in securities are subject to investment risk, including possible loss of principal. Prices of securities may fluctuate from time to time and may even become valueless. This information has not been tailored to suit any individual.

S&P 500 Trailing 5 Year Performance

Source: FactSet

Excessive Volatility in Our Future?

There has been a lot of chatter recently suggesting the potential for an excessively volatile stock market over the next several months. Many market pundits and prognosticators believe current market levels which are near all-time-highs, represent unwarranted optimism for an economy that is still struggling with the coronavirus pandemic. They believe that the current stock market level is unhinged from the reality of underlying corporate and economic fundamentals, possibly subjecting stocks to a near-term future of excessive volatility and poor returns. Chief among the supposed threats to the stock market include continued poor economic data as corporations and individuals struggle regardless of a Stimulus 2.0; that cold weather will lead to yet another spike in COVID-19 (and ensuing economic disruptions) cases especially as a vaccine fails to reach the market in a timely manner; or that the presidential race will be to too close to call on election day or may even be contested, leading to weeks or months of confusion and political turmoil.

Investing involves risk including the potential loss of principle. No investment strategy can guarantee a profit or protection against loss in periods of declining value. Past performance does not guarantee future results. Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

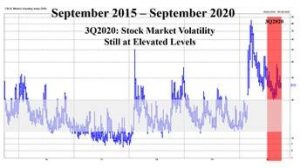

CBOE VIX Trailing 5-Year Performance

Source: FactSet

What Do We Think?

We’ve no doubt that stock markets generally appear to be long-in the tooth. We believed this before the coronavirus impact, and we certainly believe it now as most stock market indices flirt with record highs. But we do not make macro bets or utilize stock market (“index”) mutual funds or exchange-traded funds (“ETFs”). We prefer the precision of owning individual stocks where we have a greater deal of confidence in our ability to determine valuations, more easily distinguish between fundamental and non-fundamental threats to the stocks we follow and can cherry-pick the quality of the companies we invest in. We also believe that the stock market has been and continues to be excessively volatile (albeit at lower levels experienced in the spring; please refer back to the CBOE-VIX chart above) despite its strong third-quarter performance. Lastly, valuation concerns for the stock market generally have less meaning for our client’s individual and customized stock portfolios that are generally undervalued on both relative and absolute terms (although we acknowledge that volatility is sometimes contagious and can spread to all corners of the market).

How Do We Prepare for it?

The quick answer is that we don’t. We do not “prepare” our clients for such events because we believe the act of preparing for such an event involves speculation. As our readers know, we do not speculate or try to time the market as we view these schemes as short-term in nature (as opposed to our long-term investment strategy) and inherently have a low probability of adding value. Importantly, we do not keep our heads in the sand and ignore the macro events that affect stocks generally. We are not ignorant of such noise. Rather, we try to be cognizant of how the noise affects the investments we own or would like to own. We calmly and continually keep an eye on the broader markets and monitor how our portfolios and the universe of stocks we follow are affected. To the extent that the investment we care about is affected in a non-fundamental way (and do not represent a permanent impairment to our investment thesis for them), we will seek to capitalize on this short-term investment opportunity and invest for the long term. So, our typical game plan is to wait for the event to unfold. We then wait for the market to over-react as it oftentimes does. This is what we refer to as short-term market inefficiency. We will exploit this inefficiency when the opportunity presents itself and hope to receive value add over the long-term.

Investment Strategy

We seek to exploit stock market volatility in the short term through a long-term, active investment management strategy that purchases higher-quality stocks with sustainable competitive advantages and economic moats, and at prices below our calculation of intrinsic value (otherwise known as “value investing”). These characteristics help us defend against what we believe is the biggest risk in investing: a permanent loss of capital. In addition, we intend to show our discipline and conviction in our investments by employing a concentrated portfolio mandate that is differentiated and allows us to focus on only the best investment candidates available. Further, we seek to show our conviction through our portfolio weighting scheme which skews exposure to the best investment candidate.

- Active investment management

- Long-term investing

- Seek higher quality opportunities

- Value investing

- Avoid permanent losses of capital

- High conviction

- Invest with confidence

- Disciplined approach

- Volatility is an opportunity

- Concentrated stock portfolio

- Differentiated from the index

“Risk is not inherent in an investment; it is always relative to the price paid. Uncertainty is not the same as risk. Indeed, when great uncertainty – such as in the fall of 2008 – drives securities prices to especially low levels, they often become less risky investments.” — Seth Klarman

“We don’t have to be smarter than the rest. We have to be more disciplined than the rest.” — Warren Buffett

Want to learn more about our Chief Investment Office? Check out Tim’s Bio!

Questions and Consultations

If you have questions or if you’d like to schedule an appointment to discuss your finances, contact us today.

Want more information? Sign up to receive our monthly e-newsletter here.

Partnership Wealth Management is a comprehensive financial services company. We are committed to providing our clients with financial planning and wealth management services to help them make the most of their investments. At Partnership Wealth Management we have a long history of working with the LGBT community. Among our many services, we offer financial planning for gay couples and lesbian couples as well as estate planning for gay couples and lesbian couples. Financial planning is an important part of preparing for the future, contact us today to get started: www.partnershipwm.com. We always try and provide the best information – We are not responsible for information on third-party sites. Thanks for reading!