Q4 2022 Passionate Investor

A recession on the horizon?

Over the past few years, market chatter has rotated among concerns of inflation, rising interest rates, and a recession. Most of the talking heads see the worst of inflation behind us and anticipate a potential end to rising interest rates in the near future. The discussions have now begun to focus on the potential for a recession in the year ahead.

Given the years of growth we’ve seen, a recession as a possibility should not be surprising. Increasing interest rates, especially in response to high inflation, can result in a recession if executed in the extreme (seven straight interest rate increases- with four being an unusually high .75%- may qualify as extreme). Central banks are not known for their ability to guide the economy smoothly. Also, our old friend, the (inverted) yield curve, has been predicting a recession for much of the past year (please click HERE for a more in-depth discussion we previously had about yield curves).

Are we already in a recession?

The National Bureau of Economic Research (“NBER”) is the group of economists who meet to determine the official beginning and end date of recessions. Decisions are made after a recession has begun (they do not forecast), and a complete decision, including revisions, may not be completed until after the recession is over. Typically, the NBER uses several data points in determining a recession, but as we understand it, there is no official litmus test or secret sauce. In recent years, the definition of what constitutes a recession has been a little fluid (the COVID recession comes to mind). Two consecutive quarters of negative GDP growth is typically mentioned as one of those data points; however, the NBER says it is not an overriding factor, and its occurrence doesn’t always mean that an official recession has started.

Although an official recession hasn’t yet been called, it is possible that an unofficial recession started last year. Keep in mind that we did experience two consecutive quarters of negative GDP growth in 2022 (again, no guarantee of an official recession). Also, it’s possible for certain areas of our economy to flourish while others struggle. In mid-2020, housing-related industries, automotive sales, and technology companies saw record returns, while the hospitality and energy industries suffered. We’re now seeing the reverse of that early trend. Additionally, in an economy where experiences are varied between the rich and the poor, 40-year highs in inflation could affect some more than others. Despite rising wages, many households are struggling, and they have arguably been living in a non-technical recession for years- their costs are higher than they’ve ever been, and their wallets are stretched.

Even if elements of our economy feel recessionary pain, it’s possible that an official recession isn’t announced. One factor that could get in the way of an official recession is historically low unemployment and the resilient job market in the face of rising interest rates keeping the economy afloat. Another is that the official determination of recession seems to be open to error when it is decided upon by people.

What about the stock market?

Those who believe we’ll enter a recession this year predict lower lows with continued volatility in 2023. Many believe last year’s low was only a hint of what’s to come, and they point to the fact that a stock market low has never been reached prior to an official recession being announced.

Of course, other possibilities exist. We could have already reached market lows if a recession had started last year. It’s also possible that this is the most anticipated recession of all time, allowing the stock market time to adjust its pricing.

As we monitor the economic and market news, it seems that most market forecasters expect a short and shallow recession over the next year. Again, we may already be in an unofficial recession. While we are not supporting one viewpoint or another, our experience tells us to be careful when everyone seemingly all but guarantees an economic outcome. While we acknowledge the chance of our dipping into a recession at some point, nobody knows for sure, and we certainly don’t attempt to predict such things.

Regardless of your thoughts on the economy or markets in the near term, investing in the stock market is for the long-term investor. Remember, volatility is part of investing. Don’t let volatility create an oversized emotional reaction that leads you astray from your long-term focus and goals. This volatility represents opportunity over the long term.

Closing Remarks

In 2022, market forecasting was about as useful and successful as weather forecasting (our analogy). No one has an information advantage when it comes to the future. If so, fortune telling would be called future telling. Prognosticators make their forecasts by reading the tea leaves, which are in plain sight to everyone- it’s all in the interpretation. So, is it all that surprising that market prognosticators are about as accurate as fortune tellers? Not really, in our opinion. We prefer the logic of our investment strategy, which we believe can (but not guarantee) add value for investors with a long-term investment time horizon.

Having the ability to actively manage our portfolios and deviate from the broader stock market is our “Raison D’être” or reason for being (excuse our French). Being active managers at least allows us a chance to outperform the market (or shoot ourselves in the foot) in an otherwise bleak year. For those of us who experienced a challenging year, it’s important to understand that one year is too short a period to judge performance, especially if you have a long-term time horizon. Over the long-term, poor results in any year are hopefully overshadowed by many years of better returns, allowing us to potentially reach our goals. But there we go again – always the optimist. Tigers cannot change their stripes. We wish everyone a wonderful, healthy, and fruitful 2023. Please contact us if you have any questions or needs. All the best.

Market Review*

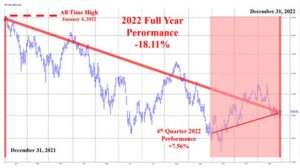

- Equity markets generally outperformed fixed-income markets, with the S&P 500 rising 7.56% (including dividends; -18.11% YTD) and the Barclay’s Capital U.S. Aggregate Bond index rising 1.87% (-13.01% YTD).

- Small caps underperformed large cap stocks (S&P 500) as the Russell 2000 small cap stock index returned +6.23% (-20.44% YTD).

- Value outperformed Growth during the quarter and full year (as determined by the S&P 1500 broad market index, which includes large, mid, and small capitalization stocks).

- International or developed, non-U.S. equity markets outperformed U.S. markets in both U.S. dollars (MSCI EAFE**: +17.40%; -14.01% YTD) and in local currency terms (+8.77%; -6.52% YTD).

- The MSCI Emerging Markets Index underperformed developed, non-U.S. equity markets (international) in both U.S. dollar (+9.79%; -19.74% YTD) and local currency terms (+6.66%; -15.16% YTD).

- Most U.S. market sectors were positive during the quarter. Energy (+22.81%; +65.72% YTD) and Industrials (+19.22%; -5.48% YTD) stocks were most distinguishable given their strength. Consumer Discretionary stocks were notable given their weakness (-10.18%; -37.03% YTD).

- High-yield bonds rose 7.97% during the quarter (-12.71% YTD). The U.S. corporate bond sector climbed 3.31% during the quarter (-15.15% YTD). 10-Year U.S. Treasury yields climbed slightly from 3.86% at the beginning of the quarter (1.44% at the beginning of the year) to 3.87% currently.

- The Japanese Yen (+8.84%; -14.58% YTD), the Euro (+8.94%; -6.15% YTD), and the British Pound (+7.76%; -11.19% YTD) all rose versus the U.S. dollar during the quarter.

* Unless otherwise noted, performances stated above reflect data provided by Standard and Poor’s, Russell Investments, MSCI, and Barclay’s Capital.

** The MSCI EAFE Index is a large capitalization, developed market benchmark that tracks non-U.S. or international equity markets.

The S&P 500 rose +7.56% during the quarter but still closed out 2022 with its worst performance since 2008. Most other stock segments (i.e., small caps, international; etc.) similarly recaptured lost ground in the 4th quarter and recorded large losses for the year. Unlike in 2021 when inflationary concerns were still debatable between transitory (those who believed that inflationary pressures were short-term in nature) and secular camps (those who believed the inflationary pressures were more longer-term in nature), market participants have generally accepted the latter. The U.S. Federal Reserve (the “Fed”) was a member of the former and has since had to play catch up with the inflation reality on the ground that has not been higher in over 40 years. Persistent COVID-related supply chain disruptions and the unexpected Russian invasion of Ukraine have exacerbated the problem with rising prices. In response, the Fed raised interest rates seven times in 2022 and has signaled that it plans more tightening measures in 2023 to bring already moderating (though still rising) inflation levels into its range of comfort.

Perhaps the most surprising story of the year is that the bond market (as measured by the Barclay’s Capital U.S. Aggregate Bond index) fell by double digits. Almost as surprising was the timing of the weakness, which occurred during a period of significant stock market losses. Investors typically look towards fixed-income investments as a safe harbor in times of stock market or economic uncertainty. Though bonds also had a reprieve during the quarter (+1.87%), they did not offer safe harbor in 2022 (-13.01%). Likewise, bonds with (i.e., corporates, high yield, etc.) and without (i.e., U.S. Treasury notes) credit exposures (which resemble stock risks) rebounded during the quarter but underperformed over the full year. The 10-year U.S. Treasury note in particular was reported to have had its worst year of performance in over 200 years. Similarly, most international currencies rose during the quarter relative to the U.S. dollar but fell considerably over the full year (relative to the U.S. dollar) as international investors were attracted to rising interest rates and the comparative safety of the dollar.

“You have enemies? Good.

It means you’ve stood up for something, sometime in your life.”

— Winston Churchill